416.889.7791

Laura@LauraQuinn.ca

About Me

About Laura

Contact

Buying

Why Buy With Me

Buyer’s Guide

Daily Listings Reports

Selling

Why Sell With Me

Seller’s Guide

How’s the Market In Toronto

Properties

Property Search

Neighbourhoods

Blog

About Me

About Laura

Contact

Buying

Why Buy With Me

Buyer’s Guide

Daily Listings Reports

Selling

Why Sell With Me

Seller’s Guide

How’s the Market In Toronto

Properties

Property Search

Neighbourhoods

Blog

August 16, 2021 |

Uncategorized

| No Comment

July 2021 Market Update

July 15, 2021 |

Uncategorized

| No Comment

June 2021 Market Update

June 14, 2021 |

Uncategorized

| No Comment

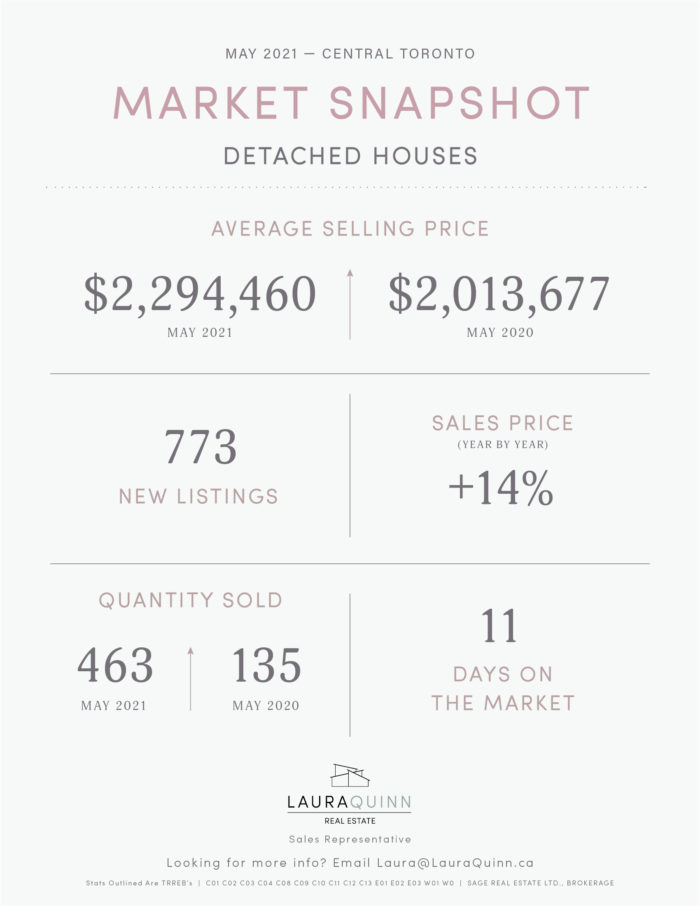

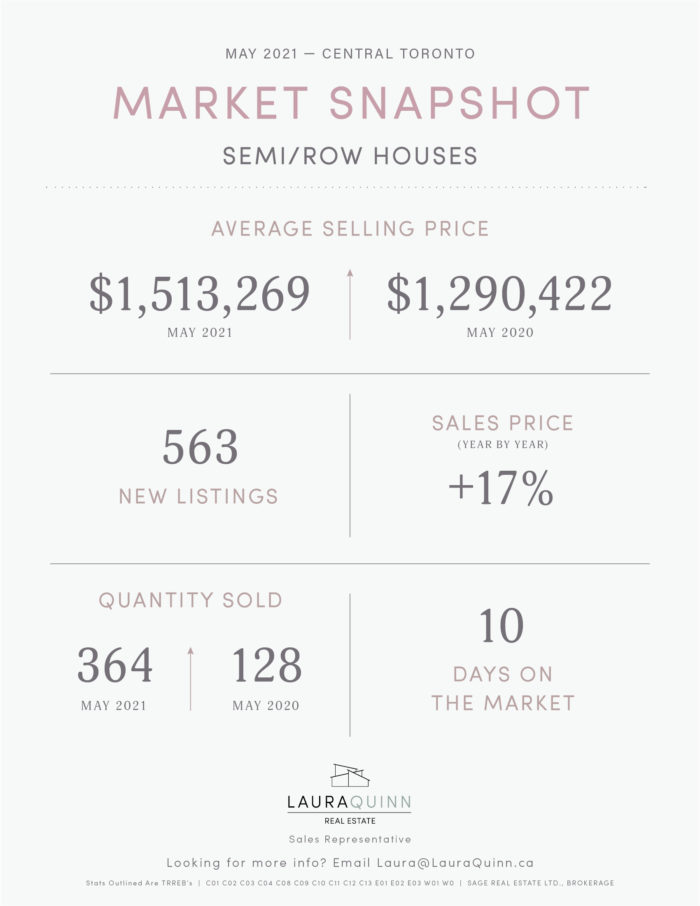

May 2021 Market Update

May 8, 2021 |

Uncategorized

| No Comment

April 2021 Market Update

April 8, 2021 |

Uncategorized

| No Comment

March 2021 Market Update

March 5, 2021 |

Uncategorized

| No Comment

February 2021 Market Update

February 11, 2021 |

Uncategorized

| No Comment

January 2021 Market Update

January 13, 2021 |

Uncategorized

| No Comment

December 2020 Market Update

December 9, 2020 |

Uncategorized

| No Comment

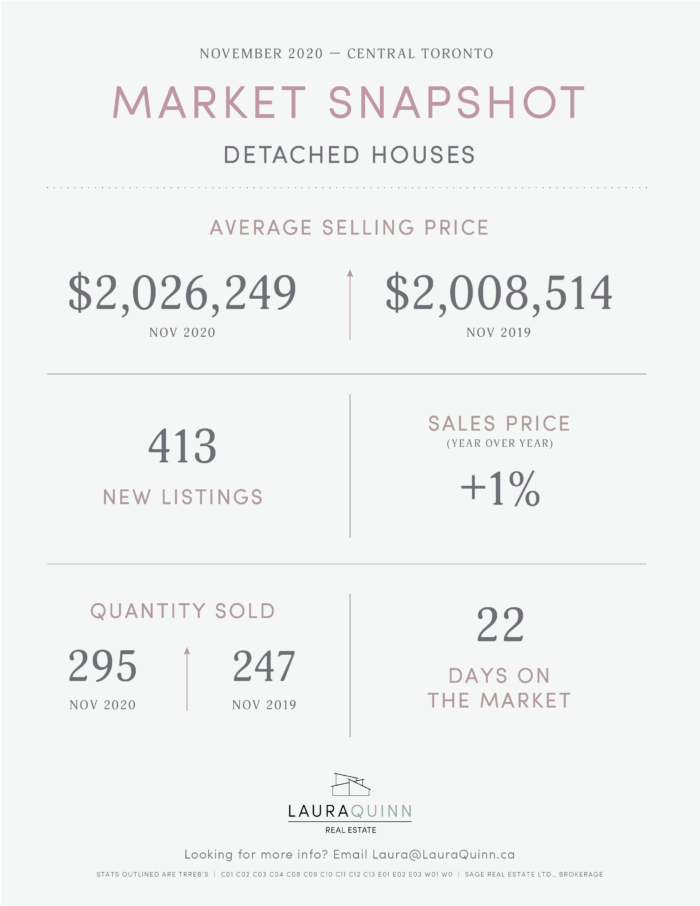

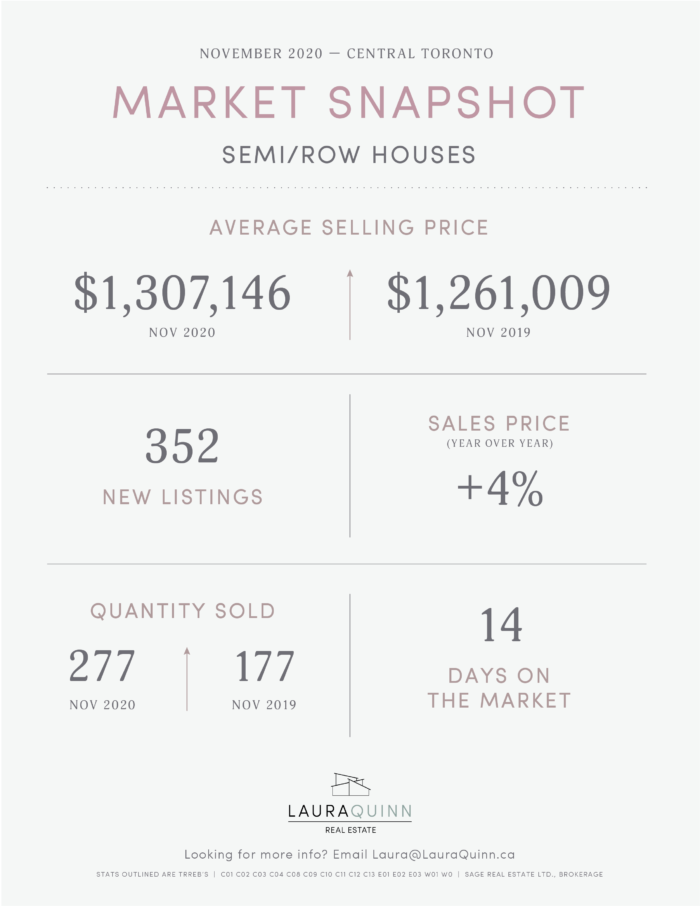

November 2020 Market Update

November 12, 2020 |

Uncategorized

| No Comment

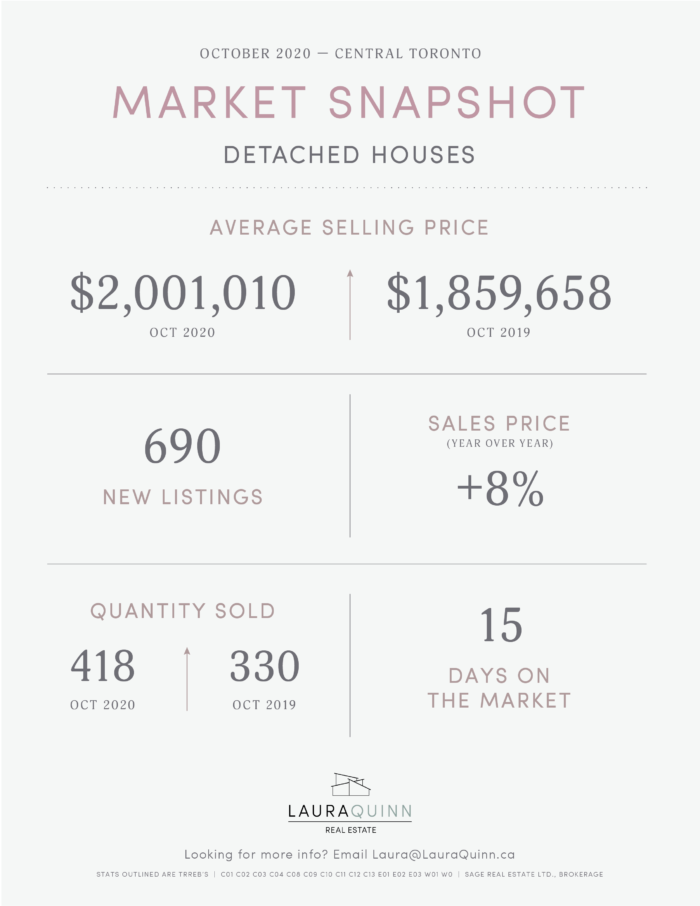

October 2020 Market Update

1

2

3

4

→

Recent Posts

July 2021 Market Update

June 2021 Market Update

May 2021 Market Update

April 2021 Market Update

March 2021 Market Update

Recent Comments

Archives

August 2021

July 2021

June 2021

May 2021

April 2021

March 2021

February 2021

January 2021

December 2020

November 2020

October 2020

April 2020

March 2020

February 2020

January 2020

April 2019

March 2019

February 2019

January 2019

December 2018

November 2018

October 2018

September 2018

August 2018

September 2017

April 2017

November 2016

Categories

Buying

Selling

Uncategorized

Meta

Log in

Entries feed

Comments feed

WordPress.org